Maximizing RRSP & TFSA Contributions Without Overcontributing

Jason Primmer - Mar 02, 2026

With the RRSP deadline now behind us, it is a good time to review your RRSP and TFSA contribution room to ensure you are maximizing tax advantaged savings while avoiding overcontribution penalties.

Following up on our February newsletter, and with the RRSP deadline now behind us, it is worth revisiting how investors can ensure they are maximizing RRSP and TFSA contributions without overcontributing.

RRSP Contribution Room

RRSP contribution room is accumulated each year you earn employment income. You receive 18% of your previous year’s employment income as RRSP room. For example, if you earned $100,000 in 2024, you would get $18,000 in new RRSP room in 2025. Note that there is a year delay, so if you are a new resident, or starting your first job, you may not have RRSP room yet. However, for the rest of us, you’ll have accumulated room from working the previous year, plus you get to carry forward any room earned in previous years that you have used yet.

The timing for RRSP contributions is a little bit different from the typical calendar year. To have your contributions count for the given year (e.g. 2025), you have an extra 60 days each year. This is usually March 1st but depends on whether it’s a leap year or if March 1st falls on a weekend. February 29th would be the deadline in a leap year, and March 2nd is the deadline in 2026 since the 1st falls on a Sunday. Contributions made during the first 60 days of the year can be used in two ways: for the previous tax year or the current tax year.

Looking up your RRSP Contribution Room

You can confirm your RRSP room (including any carry forward room you might have) on your Notice of Assessment, which you receive after you file your taxes. Your 2024 Notice of Assessment will show your available RRSP contribution room for 2025.

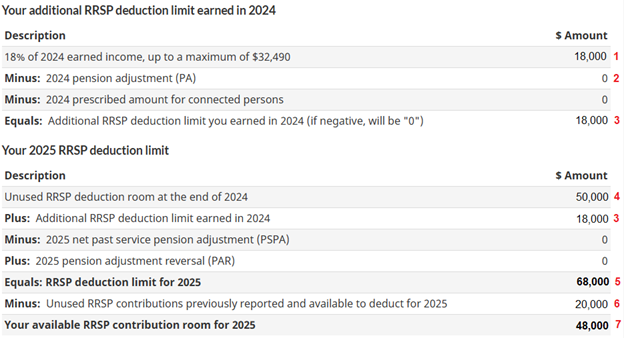

Let’s look at a sample Notice of Assessment:

The below outlines the new RRSP room section of a Notice of Assessment:

- This is the amount of new room earned based on your earned income (e.g. employment income, rental income). As discussed previously, it is 18% of your income.

- If you have a registered pension plan (like a defined benefit pension plan or a defined contribution pension plan), you will likely receive a pension adjustment for pension contributions made by yourself and/or your employer. These are listed on your T4. They do not reduce your current year’s RRSP room but rather reduce next year’s available room. Employer matching plans come in many different flavours – some contributions count as regular RRSP contributions in the current year and others are factored into a pension adjustment – so it’s important to understand your own plan and how those contributions affect your new room.

- The amount your contribution room is increasing for the year.

- Unused RRSP deduction room at the end of 2024 – this is RRSP room that you have not deducted from your taxes yet. It contains a mix of unused contribution room and unused deductions, if any (see point 6 for further information).

- Your RRSP deduction limit for 2025 is how much you are allowed to deduct from your taxes in the year 202 On its own, it’s not a very useful number, aside from how much you could potentially reduce your income by in 2025. For example, if you had an income of $200,000 in 2025, you could, through RRSP contributions, reduce that to $132,000 in taxable income.

- Unused RRSP contributions previously reported and available to deduct for 2025 includes amounts that you have already put into your RRSP account and received a contribution slip for and reported on your tax return. However, these amounts have not be deducted from your income yet and could be used to reduce your income in future years.

- Your available RRSP contribution room for 2025 is the amount that you are allowed to contribute to your RRSP for the 2025 year. Remember: these contributions can be made until the first 60 days of the year (i.e. March 2, 2026 for this year). If you contribute more than this amount, you may incur penalties of 1% of the overcontribution per month.

Why Would I Have Unused RRSP Contributions?

There are 2 main reasons why this may be the case:

The first is that you contributed to your RRSP account, but didn’t want to reduce your taxes in that year. This might happen if someone knows that they will jump up into a higher tax bracket in a subsequent year and they want to use the RRSP deduction when their income is much higher. As an investor, you’ll have to weigh the higher tax deduction in later years with being able to invest more (i.e. tax refund), a year or more earlier and the compound growth earned on that tax refund.

The second reason you might have unused contribution room is if you contributed in the first 60 days of the year, but you didn’t have enough contribution room for the amount you added to the RRSP. For example, let’s say that you had $10,000 in contribution room for 2024. You added $10,000 before the end of the year. Then in January of 2025 you started a new job with a contribution matching plan and you and your employer contributed $3,000 to the plan during the first 60 days, which counted as RRSP contributions (not pension adjustments). Since you’ve already maximized your room for 2024, you aren’t able to deduct the $3,000 from your income, so that becomes an unused RRSP contribution. You still report it on your taxes in 2024, because you received the RRSP contribution receipt for your 2024 taxes. However, because the extra $3,000 was contributed in 2025, you can use that against the new room you’ll earn in 2025, which technically you get at the beginning of January, even if you don’t know the exact amount until you file your taxes. In this example, there is no overcontribution and no penalty if your new 2025 room is above $3,000. If however, you added the $3,000 before the end of the year, then you would have overcontributed by $3,000 and would owe penalties. The CRA offers a buffer of $2,000, so you would owe penalties on the $1,000 difference – 1% for each month the extra $1,000 was in the account.

Looking Up RRSP Room on CRA’s MyAccount

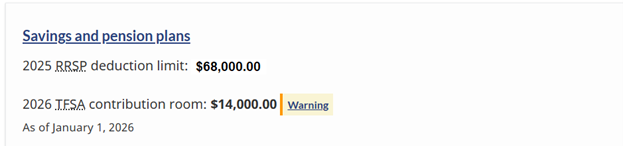

My biggest annoyances with the CRA MyAccount is that CRA only reports the deduction limit on the home page. If you don’t have any unused contributions, this is fine. However if you do have unused contributions, this can easily cause overcontributions and penalties.

Using our earlier example, when you log onto CRA, you only see the deduction limit of $68,000, which we now know is not necessarily the same as the amount you are allowed to contribute, which was only $48,000. If you have unused contributions, and contributed based on the $68,000 below, you’d have a $20,000 overcontribution and a penalty of $200 per month!

Therefore, I always suggesting looking at your Notice of Assessment when checking your RRSP room and ignoring the home page of CRA’s MyAccount.

TFSA Contribution Room

Looking up your TFSA contribution room in CRA’s MyAccount can also be problematic. The reason for this is that financial institutions generally only send contribution amounts to the CRA once per year, at the end of February (similar to a T4 sent by your employer at tax time). As a result, when you check your room early in the year, it might show a higher limit than what you actually have, because it hasn’t incorporated contributions from the previous year yet. The same goes for any contributions made in the current year. CRA won’t have those contributions until the end of the year either. Therefore, its important to track TFSA contributions outside of CRA, check what contributions and withdrawals CRA is using to calculate your available room, and use the available room on the home page with caution.

For clients of Daley Wealth Management, we help you track these amounts regularly to make sure that you are topping up your accounts as much as possible, without going over and incurring penalties.